Implied Volatility (IV) and Vega are very much related but are by no means the same thing.

Implied volatility has no direct correlation to actual past historical or statistical volatility; rather it is a measure of predicted future movement. Implied volatility tends to increase when there is uncertainty or anticipated news, while it tends to decrease in times of calm.

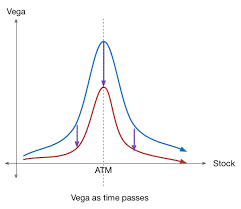

Vega measures the amount of increase or decrease in premium based on a 1% (100 basis points) change in the implied volatility assumption. Longer-term options tend to have higher Vega than near-term options. Longer-termed options are typically more expensive, and a 1% change in implied volatility will represent a larger dollar amount of that premium than an option with a lower premium.

Follow me on Twitter @MikeShorrCbot